Forecasting using ARml model

Value

A list class of forecast containing the following elemets

x : The input time series

method : The name of the forecasting method as a character string

mean : Point forecasts as a time series

lower : Lower limits for prediction intervals

upper : Upper limits for prediction intervals

level : The confidence values associated with the prediction intervals

model : A list containing information about the fitted model

newxreg : A matrix containing regressors

Examples

library(caretForecast)

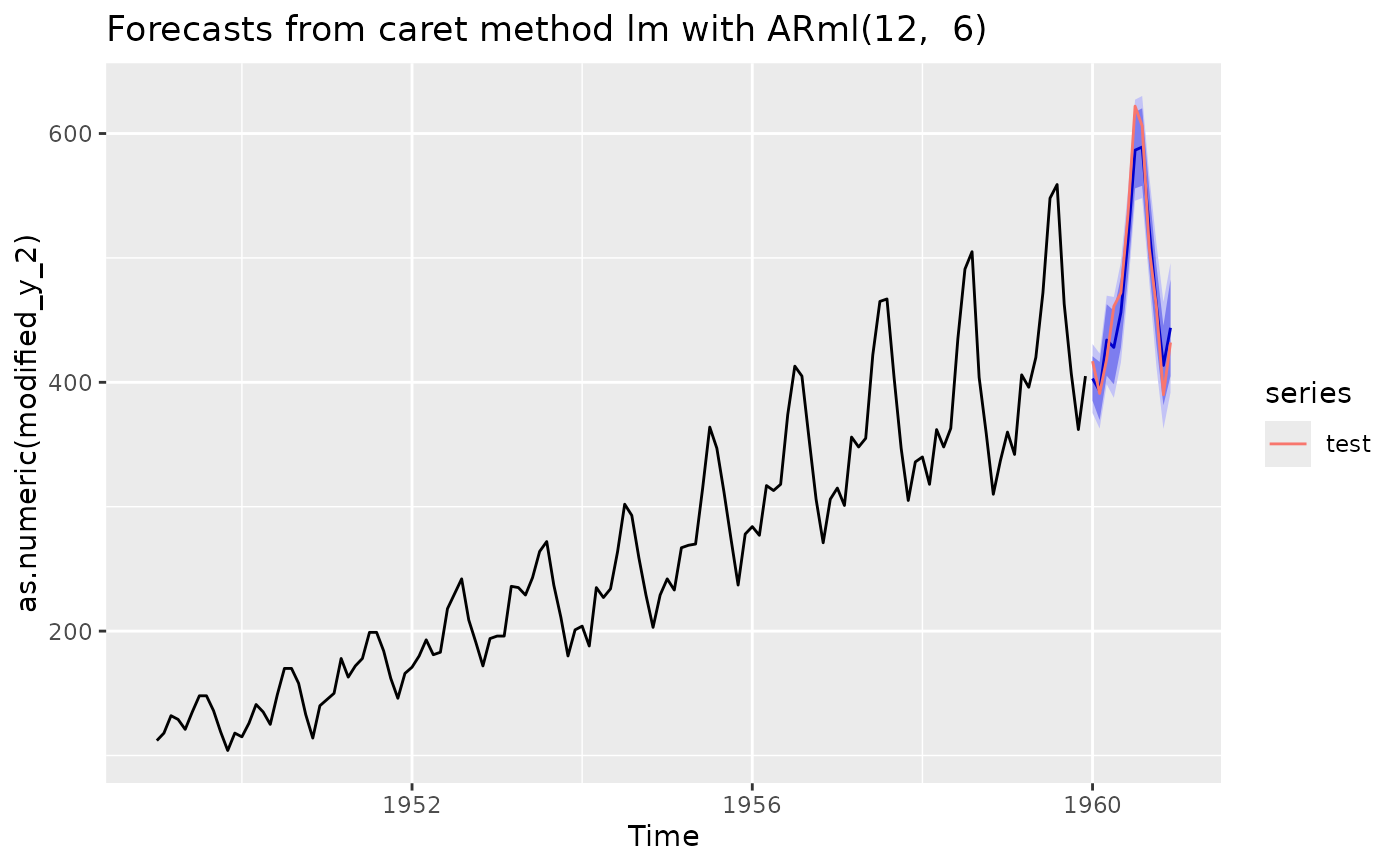

train_data <- window(AirPassengers, end = c(1959, 12))

test <- window(AirPassengers, start = c(1960, 1))

ARml(train_data, caret_method = "lm", max_lag = 12) -> fit

#> initial_window = NULL. Setting initial_window = 112

#> + Training112: intercept=TRUE

#> - Training112: intercept=TRUE

#> + Training113: intercept=TRUE

#> - Training113: intercept=TRUE

#> + Training114: intercept=TRUE

#> - Training114: intercept=TRUE

#> + Training115: intercept=TRUE

#> - Training115: intercept=TRUE

#> + Training116: intercept=TRUE

#> - Training116: intercept=TRUE

#> Aggregating results

#> Fitting final model on full training set

#> Performing horizon-specific calibration for conformal prediction intervals...

#> Calibrating conformal scores using 34 rolling windows...

#> Calibration complete. Samples per horizon: 34 to 34

forecast(fit, h = length(test), level = c(80,95)) -> fc

autoplot(fc)+ autolayer(test)

accuracy(fc, test)

#> ME RMSE MAE MPE MAPE MASE

#> Training set -6.039671e-15 10.19861 7.884296 -0.1380603 3.263387 0.2589260

#> Test set 5.515070e+00 19.71858 17.108979 0.8260714 3.540353 0.5618712

#> ACF1 Theil's U

#> Training set 0.07296876 NA

#> Test set 0.32299513 0.3864957

accuracy(fc, test)

#> ME RMSE MAE MPE MAPE MASE

#> Training set -6.039671e-15 10.19861 7.884296 -0.1380603 3.263387 0.2589260

#> Test set 5.515070e+00 19.71858 17.108979 0.8260714 3.540353 0.5618712

#> ACF1 Theil's U

#> Training set 0.07296876 NA

#> Test set 0.32299513 0.3864957