Autoregressive forecasting using various Machine Learning models.

Usage

ARml(

y,

max_lag = 5,

xreg = NULL,

caret_method = "cubist",

metric = "RMSE",

pre_process = NULL,

cv = TRUE,

cv_horizon = 4,

initial_window = NULL,

fixed_window = FALSE,

verbose = TRUE,

seasonal = TRUE,

K = frequency(y)/2,

tune_grid = NULL,

lambda = NULL,

BoxCox_method = c("guerrero", "loglik"),

BoxCox_lower = -1,

BoxCox_upper = 2,

BoxCox_biasadj = FALSE,

BoxCox_fvar = NULL,

allow_parallel = FALSE,

calibrate = TRUE,

calibration_horizon = NULL,

n_cal_windows = NULL,

...

)Arguments

- y

A univariate time series object.

- max_lag

Maximum value of lag.

- xreg

Optional. A numerical vector or matrix of external regressors, which must have the same number of rows as y. (It should not be a data frame.).

- caret_method

A string specifying which classification or regression model to use. Possible values are found using names(getModelInfo()). A list of functions can also be passed for a custom model function. See https://topepo.github.io/caret/ for details.

- metric

A string that specifies what summary metric will be used to select the optimal model. See

?caret::train.- pre_process

A string vector that defines a pre-processing of the predictor data. Current possibilities are "BoxCox", "YeoJohnson", "expoTrans", "center", "scale", "range", "knnImpute", "bagImpute", "medianImpute", "pca", "ica" and "spatialSign". The default is no pre-processing. See preProcess and trainControl on the procedures and how to adjust them. Pre-processing code is only designed to work when x is a simple matrix or data frame.

- cv

Logical, if

cv = TRUEmodel selection will be done via cross-validation. Ifcv = FALSEuser need to provide a specific model viatune_gridargument.- cv_horizon

The number of consecutive values in test set sample.

- initial_window

The initial number of consecutive values in each training set sample.

- fixed_window

Logical, if FALSE, all training samples start at 1.

- verbose

A logical for printing a training log.

- seasonal

Boolean. If

seasonal = TRUEthe fourier terms will be used for modeling seasonality.- K

Maximum order(s) of Fourier terms

- tune_grid

A data frame with possible tuning values. The columns are named the same as the tuning parameters. Use getModelInfo to get a list of tuning parameters for each model or see https://topepo.github.io/caret/available-models.html. (NOTE: If given, this argument must be named.)

- lambda

BoxCox transformation parameter. If

lambda = NULLIflambda = "auto", then the transformation parameter lambda is chosen usingBoxCox.lambda.- BoxCox_method

BoxCox.lambdaargument. Choose method to be used in calculating lambda.- BoxCox_lower

BoxCox.lambdaargument. Lower limit for possible lambda values.- BoxCox_upper

BoxCox.lambdaargument. Upper limit for possible lambda values.- BoxCox_biasadj

InvBoxCoxargument. Use adjusted back-transformed mean for Box-Cox transformations. If transformed data is used to produce forecasts and fitted values, a regular back transformation will result in median forecasts. If biasadj is TRUE, an adjustment will be made to produce mean forecasts and fitted values.- BoxCox_fvar

InvBoxCoxargument. Optional parameter required if biasadj=TRUE. Can either be the forecast variance, or a list containing the interval level, and the corresponding upper and lower intervals.- allow_parallel

If a parallel backend is loaded and available, should the function use it?

- calibrate

Logical. If TRUE, performs rolling-origin calibration to compute horizon-specific conformal prediction intervals. This produces properly calibrated intervals that widen with forecast horizon (trumpet shape). Default is TRUE.

- calibration_horizon

Maximum forecast horizon for calibration. If NULL (default), uses

2 * frequency(y)for seasonal data or 10 for non-seasonal data.- n_cal_windows

Number of rolling windows for calibration. If NULL (default), automatically determined based on data length (max 50).

- ...

Ignored.

Value

A list class of forecast containing the following elemets

x : The input time series

method : The name of the forecasting method as a character string

mean : Point forecasts as a time series

lower : Lower limits for prediction intervals

upper : Upper limits for prediction intervals

level : The confidence values associated with the prediction intervals

model : A list containing information about the fitted model

newx : A matrix containing regressors

calibration : Horizon-specific conformal calibration scores (if calibrate=TRUE)

Examples

library(caretForecast)

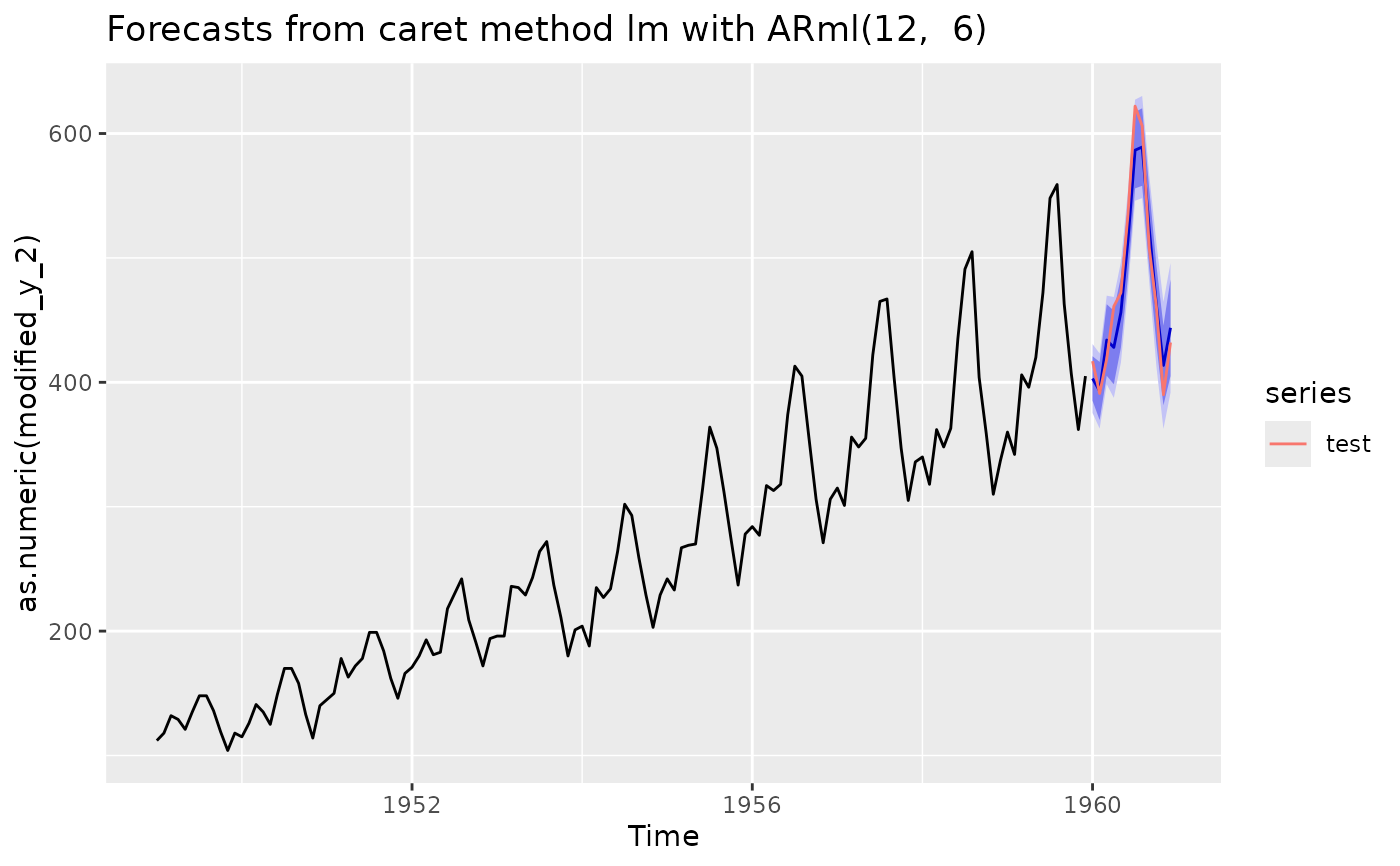

train_data <- window(AirPassengers, end = c(1959, 12))

test <- window(AirPassengers, start = c(1960, 1))

ARml(train_data, caret_method = "lm", max_lag = 12) -> fit

#> initial_window = NULL. Setting initial_window = 112

#> Loading required package: ggplot2

#> Loading required package: lattice

#> + Training112: intercept=TRUE

#> - Training112: intercept=TRUE

#> + Training113: intercept=TRUE

#> - Training113: intercept=TRUE

#> + Training114: intercept=TRUE

#> - Training114: intercept=TRUE

#> + Training115: intercept=TRUE

#> - Training115: intercept=TRUE

#> + Training116: intercept=TRUE

#> - Training116: intercept=TRUE

#> Aggregating results

#> Fitting final model on full training set

#> Performing horizon-specific calibration for conformal prediction intervals...

#> Calibrating conformal scores using 34 rolling windows...

#> Calibration complete. Samples per horizon: 34 to 34

forecast(fit, h = length(test)) -> fc

autoplot(fc) + autolayer(test)

accuracy(fc, test)

#> ME RMSE MAE MPE MAPE MASE

#> Training set -6.039671e-15 10.19861 7.884296 -0.1380603 3.263387 0.2589260

#> Test set 5.515070e+00 19.71858 17.108979 0.8260714 3.540353 0.5618712

#> ACF1 Theil's U

#> Training set 0.07296876 NA

#> Test set 0.32299513 0.3864957

accuracy(fc, test)

#> ME RMSE MAE MPE MAPE MASE

#> Training set -6.039671e-15 10.19861 7.884296 -0.1380603 3.263387 0.2589260

#> Test set 5.515070e+00 19.71858 17.108979 0.8260714 3.540353 0.5618712

#> ACF1 Theil's U

#> Training set 0.07296876 NA

#> Test set 0.32299513 0.3864957